Financial Safety Nets: Shifting From Basic Savings to Smart Emergency Planning

Life has a strange way of throwing unexpected surprises at us when we least expect them. A sudden medical bill, an urgent car repair, or a sudden change in employment can completely throw your monthly budget off track. In those stressful moments, having a financial cushion isn’t just a luxury—it is your only line of defense against falling into a dangerous debt trap.

This is where an Emergency Fund comes into play. It is a dedicated pile of cash set aside strictly for life’s unplanned crises. However, the biggest mistake most people make is simply leaving this crucial money rotting in a regular savings account, or worse, locking it up in risky market investments. Let us break down how to build a smart safety net that actually protects you.

How Much Cash Do You Really Need?

The golden rule of personal finance is to save between 3 to 6 months’ worth of your essential living expenses. Notice the word “essential.” This does not mean replacing your entire current monthly income.

To calculate your target, sit down and add up only your absolute survival costs: your rent or home loan EMI, groceries, electricity bills, basic insurance premiums, and any existing loan payments. If your monthly survival cost is $1,500, your target emergency fund should be anywhere between $4,500 and $9,000. Having this amount ready gives you total peace of mind to navigate any storm without panic.

The Trap of Regular Savings Accounts

Most individuals think they are safe because they keep extra money in their primary bank account. But a standard savings account is actually the worst place to store your emergency cash for two major reasons: temptation and inflation.

When your emergency cash is sitting in the same account you use for daily shopping, swiping your card, or ordering food online, it is incredibly easy to accidentally spend it on a “non-emergency” luxury. Secondly, regular savings accounts offer incredibly low interest rates. Over time, inflation quietly eats away at the purchasing power of your money, meaning your safety net is actually shrinking every single year.

Where Should You Actually Keep the Money?

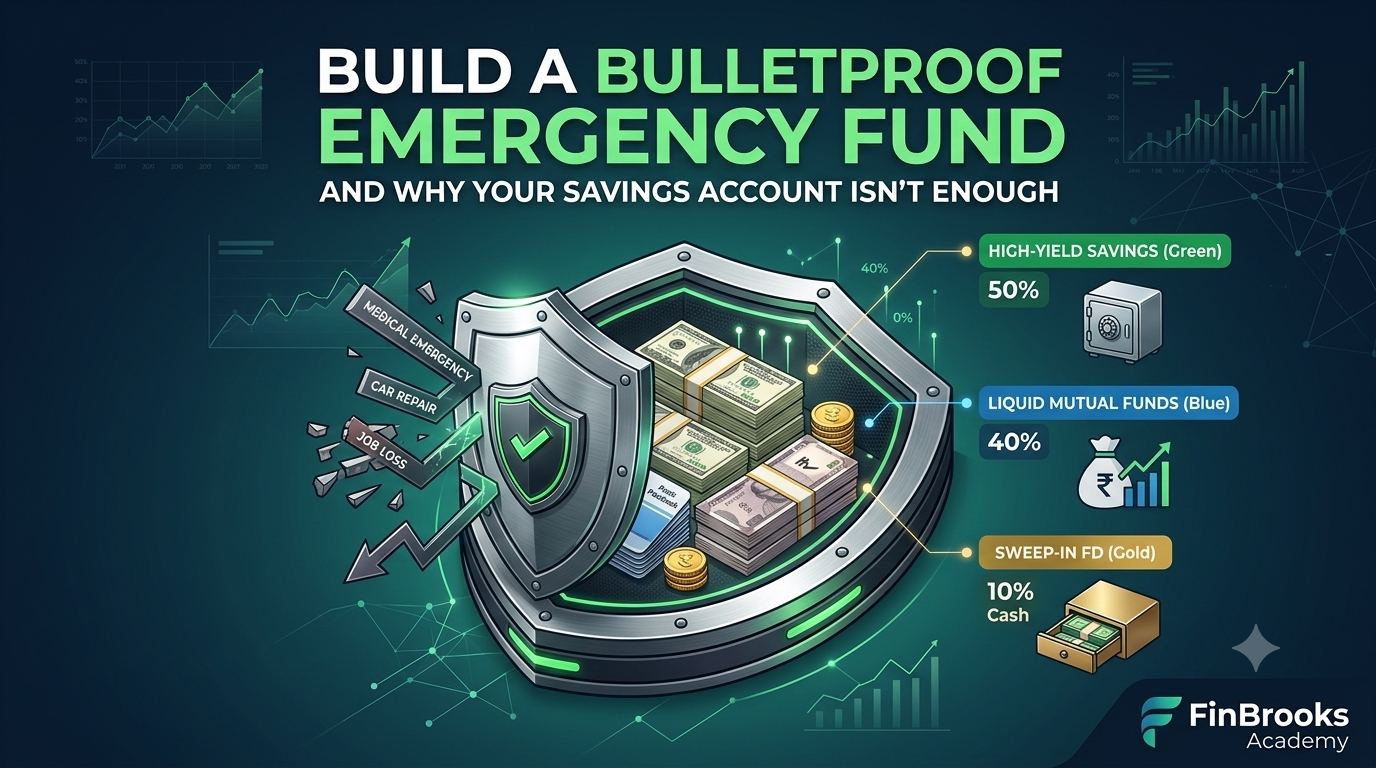

An ideal emergency fund requires a perfect balance of two things: Liquidity (how fast you can get the cash) and Safety (zero risk of losing the principal amount). You should divide your total fund into three smart buckets.

First, keep a small amount, around 10%, as hard cash at home or in your main checking account for instant access in the middle of the night. Second, move 50% into a separate High-Yield Savings Account or a Sweep-In Fixed Deposit. This keeps the money away from your daily spending vision while earning a much higher interest rate.

Finally, place the remaining 40% into Liquid Mutual Funds or Short-Term Arbitrage Funds. These funds allow you to withdraw your money within 24 hours while offering better tax-efficient returns than a traditional bank.

Comparison Matrix for Emergency Cash

| Storage Option | Accessibility Speed | Interest/Growth Potential | Risk Level |

| Cash at Home | Immediate (Instant) | Zero (Loss due to inflation) | High physical risk |

| Traditional Savings | Very Fast (ATM/UPI) | Very Low (2% to 3%) | No market risk |

| High-Yield Sweep-In FD | Fast (Same day online breakdown) | Medium (6% to 7%) | No market risk |

| Liquid Mutual Funds | Moderate (Within 24 hours) | Optimal (Better than savings) | Extremely Low |

FinBrooks Reality Check

An emergency fund is not an investment to make you rich; it is an insurance policy to keep you from becoming poor. Do not try to maximize returns on this specific money by investing it in stocks or crypto. If the market crashes on the exact day you face a personal crisis, your safety net will be cut in half.

Focus on building this shield first before you put even a single dollar into the stock market. Start small by automating a tiny transfer every month until your shield is fully formed.

Stay Ahead of the Market 📈

Subscribe to our weekly newsletter

Get your weekly market summary from FinBrooks Insights and smart financial lessons from FinBrooks Academy delivered straight to your inbox every weekend!