Guaranteed Returns: Choosing Between One-Time Savings and Monthly Habits

When it comes to keeping our hard-earned money safe, the stock market can sometimes feel like a wild roller coaster ride. That is why millions of smart savers fall back on traditional, rock-solid options offered by banks: Fixed Deposits (FD) and Recurring Deposits (RD). Both offer guaranteed returns and complete peace of mind, but they cater to two entirely different financial habits.

The big dilemma isn’t about which one is safer, both are incredibly secure. The real question is, how do you earn the absolute maximum interest based on your current cash flow? Let us break down the mechanics of both options so you can put your idle cash to work efficiently.

What is a Fixed Deposit (FD)?

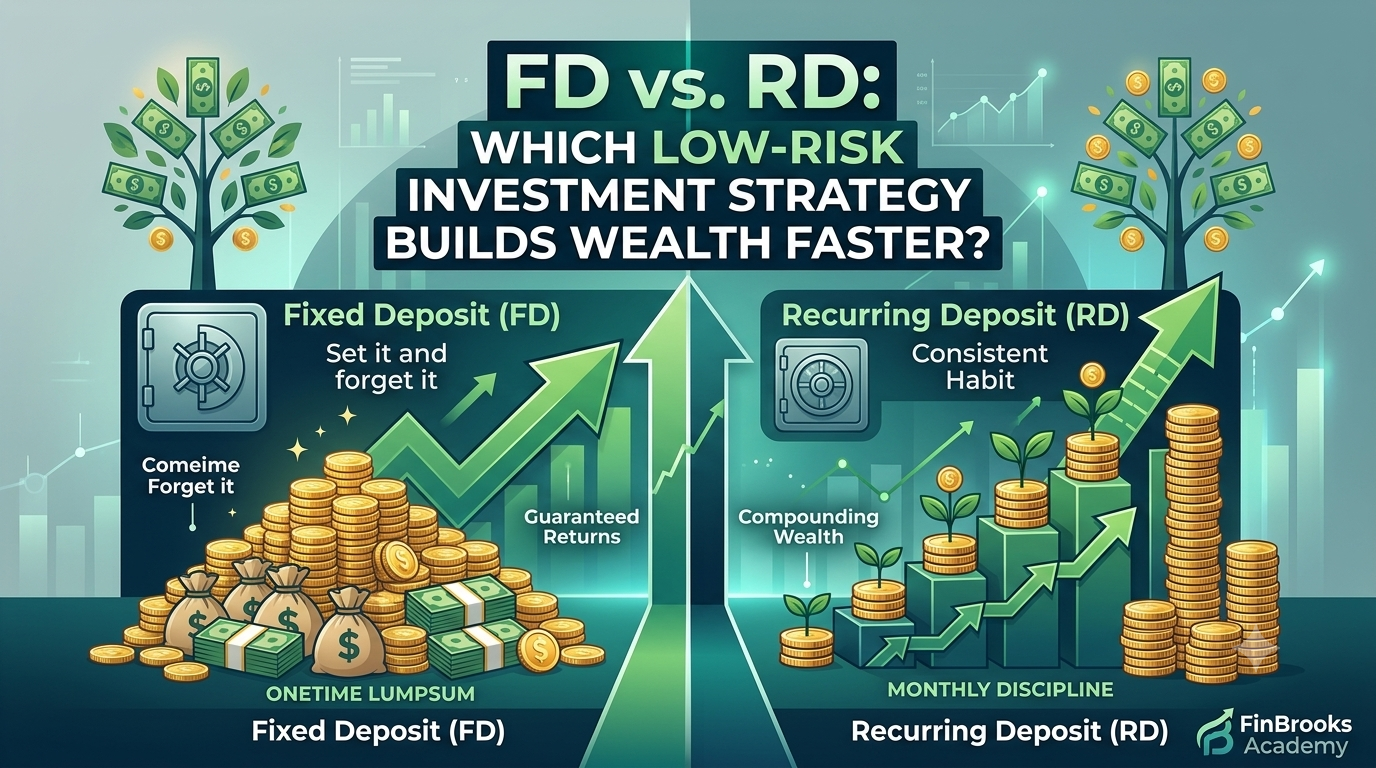

A Fixed Deposit is a one-time investment strategy. You take a lump sum of money that you do not need immediately—say, from a festival bonus or extra business profits—and lock it up with a bank for a specific period. This tenure can range from a few months to several years.

Think of an FD like planting a fully grown tree in your garden. You put it in the ground once, and it immediately starts bearing fruit at a fixed, predetermined interest rate. The bank rewards you with a higher interest rate because you promise not to touch that money until the maturity date arrives. It is the ultimate “set it and forget it” tool for lump sum cash.

What is a Recurring Deposit (RD)?

A Recurring Deposit, on the other hand, is built for monthly discipline. Instead of needing a large amount of money upfront, an RD allows you to invest a fixed, smaller amount every single month into your account.

Think of an RD like building a brick wall, one brick at a time, every month. It is ideal for salaried individuals who save a portion of their monthly paycheck. The bank locks in a fixed interest rate for the entire duration, meaning your regular monthly savings grow steadily without being affected by shifting market conditions.

The Interest Calculation Catch

Here is where many savers get confused. If an FD and an RD both offer a 7% interest rate, will they yield the same profit? The answer is a big no.

With a Fixed Deposit, your entire lump sum earns interest from day one. If you invest $10,000 in an FD, that full $10,000 compounds for the whole year.

With a Recurring Deposit, if you save $1,000 every month, only your first month’s installment earns interest for the full 12 months. Your second month’s installment only earns interest for 11 months, the third for 10 months, and so on. Because your money spends less time in the bank, the absolute interest earned at the end of the year will always be lower than a lump sum FD.

The Direct Comparison Cheat Sheet

| Feature | Fixed Deposit (FD) | Recurring Deposit (RD) |

| Deposit Style | One-time, bulk payment | Fixed monthly installments |

| Initial Capital | Requires a lump sum upfront | Can start with very small monthly amounts |

| Interest Yield | Higher total returns (money works longer) | Lower absolute returns (money enters gradually) |

| Ideal For | Windfalls, bonuses, or idle savings | Regular monthly savers and salaried earners |

| Flexibility | Premature withdrawal penalties apply | Missing monthly payments can trigger small penalties |

FinBrooks Reality Check

Choosing between an FD and an RD comes down to a simple assessment of your bank account today. Do not wait until you accumulate a massive amount of money to start saving. If your income arrives in monthly installments, open an RD immediately to build the habit of automatic, disciplined saving.

On the flip side, if you already have cash sitting idle in a basic checking account earning almost zero interest, move it into a Fixed Deposit right away. Let your money work as hard for you as you did to earn it.

Stay Ahead of the Market 📈

Subscribe to our weekly newsletter

Get your weekly market summary from FinBrooks Insights and smart financial lessons from FinBrooks Academy delivered straight to your inbox every weekend!